Introduction

If your credit report shows an account status like written-off, settled, or closed, it can change how banks judge you, even if your current income is good. In India, many loan rejections occur not because the person is “bad,” but because their credit report shows a status that signals past repayment stress.

This is why understanding the difference between written-off, settled, and closed in a credit report is important before you apply for a home loan, personal loan, or even a credit card limit increase. These words are not just labels. They tell lenders whether you fully repaid what you owed, partly repaid it, or didn’t repay, and the lender treated it as a loss.

In this guide, you’ll learn what each status means in simple language, how lenders react to it, how long these records can stay visible, and what you can practically do to improve your chances of future loan approval.

Quick Answer

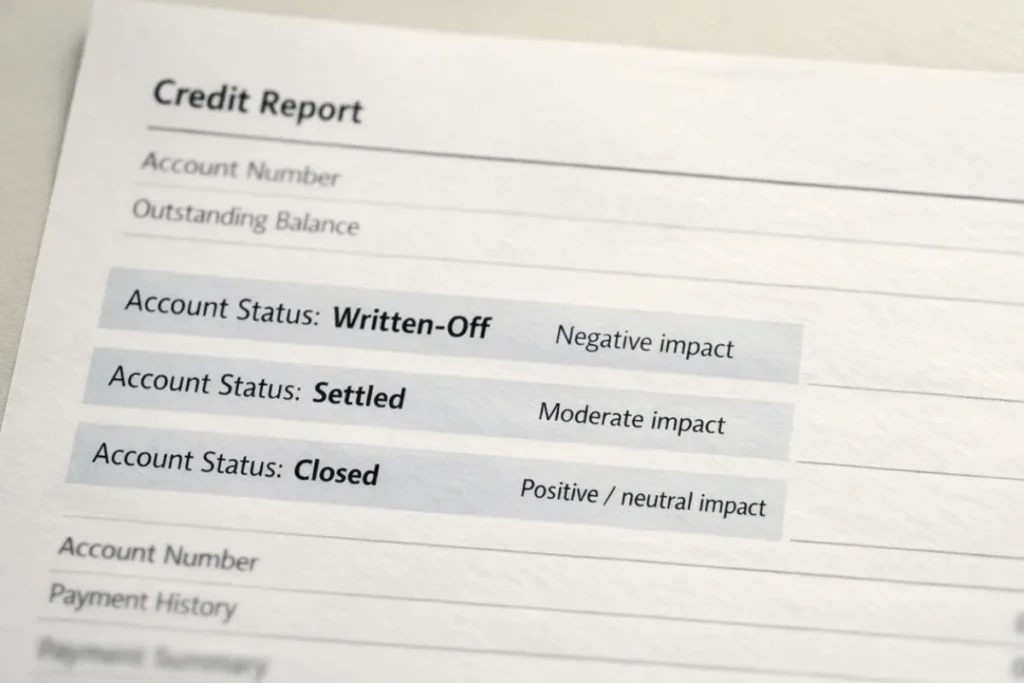

Closed means you repaid the loan in full, and the account is properly closed. Settled means you paid only part of the dues as a compromise, and the lender closed the account, but lenders treat it as risky. Written-off means the lender marked the unpaid amount as a loss, which is usually the most negative status for future loans.

What do these statuses mean in India?

What does “Closed” mean?

Closed means your dues are fully paid, and the lender has updated the account as closed. This is the cleanest outcome. It supports loan eligibility because it showsthat you completed the repayment properly.

What does “Settled” mean?

Settled typically means the lender accepted a lower amount than what you owed, as a one-time settlement/compromise. The account is closed, but not as “paid in full”. TransUnion CIBIL clearly notes that lenders view “settled” accounts as risky.

What does “Written-off” mean?

Written-off means the lender treated your unpaid loan or card dues as a loss on their books after prolonged non-payment. This is a strong negative signal and is generally viewed unfavourably by lenders.

Written-off vs Settled vs Closed: Comparison Table

| Status in credit report | What it usually means | Why it happens | How lenders see it | Future loan impact |

|---|---|---|---|---|

| Closed | Paid in full, account properly closed | Full repayment done | Positive repayment behaviour | Best chances, better rates |

| Settled | Status in the credit report | Financial difficulty, negotiated payoff | Higher risk, needs explanation | The lender treated the dues as loss |

| Written-off | The lender treated the dues as a loss | Long non-payment, default | Serious negative marker | The lender treated the dues as a loss |

How does it affect future loans in real life?

Here’s how banks typically think:

- Home loan: more strict. “Settled” or “written-off” can trigger rejection or additional conditions (a higher down payment, a co-applicant, a higher rate).

- Personal loans/credit cards: strictest. Many lenders avoid these profiles because they’re unsecured.

- Car loan: depends on profile and down payment, but negative statuses still reduce chances.

One important thing: even if a lender approves, the pricing can be worse. This is not only about approval, but also about your interest rate.

How long can these records stay visible?

In India, credit information must be retained for a minimum of 7 years under the Credit Information Companies (Regulation) Act, as stated in TransUnion CIBIL’s privacy policy.

So if your report shows a negative status today, you should plan improvement with patience. No instant fix, but steady progress works.

Case example

Amit had an old credit card due of ₹48,000. During a tough period, he paid ₹30,000 as a settlement and the card got closed as “Settled”. Six months later, he applied for a personal loan for a medical expense. Two lenders rejected him quickly because the settled status signalled past non-full repayment. After 12 months of clean payments on his active accounts and lower utilisation, he got approved with a smaller amount and a higher rate. Moral: settlement closes the pain, but it also leaves a visible mark for some time.

What to do if your report shows “Settled” or “Written-off”

Step 1: Confirm the status is correct

First, download your report and check:

- account number

- lender name

- current balance

- status (settled/written-off/closed)

- dates of last payment

If something looks wrong, dispute it.

Step 2: If you can, aim for “Closed” instead of “Settled”

If you settled earlier but still have the ability now, ask the lender:

- What is the total due to make it “paid in full”?

- Can they update the reporting to show it as closed after full payment?

Not every lender changes it, but asking is worth it. Bas yahi, practical step many people skip.

Step 3: Raise a dispute if the reporting is wrong

If the loan is actually paid in full but still shows as settled/written off, raise a dispute with the credit bureau and attach proof. CIBIL mentions disputes may take around 30 days, depending on how fast the lender responds.

Step 4: Rebuild your profile for 6–12 months

Even if the status stays, you can improve your overall profile:

- Pay every EMI on time

- Keep credit card utilisation low

- Avoid multiple new applications in a short time

- Maintain stable repayment behaviour

If you want a structured plan to improve your credit score, build it around these basics and track progress monthly.

Common mistakes people make

- Thinking “settled” is the same as “closed”. It’s not.

- Applying everywhere after a settlement and collecting too many enquiries

- Ignoring small pending charges that keep accounts from showing properly closed

- Not keeping closure letters, payment proofs, and settlement letters

- Disputing without documents, then giving up

Practical checklist before you apply for a new loan

- Check your credit report status for every account

- Ensure closed loans show Closed, andthe balance is zero

- If you see Settled/Written-off, decide on your plan:

- Can you repay and request a “paid in full” update?

- If not, wait and rebuild the profile for 6–12 months

- Keep utilisation under control

- Avoid applying to multiple lenders in the same week

- Keep proof documents ready (NOC, closure letter, settlement letter)

FAQs

Is “settled” better than “written off”?

Usually, yes, because a settlement shows you paid something and resolved the account. But lenders still treat “settled” as a risky signal because it indicates non-full repayment. If you can move towards “paid in full/closed” over time, that’s better.

Can I get a home loan with a “settled” status?

It’s possible, but harder. Many lenders will ask for a higher down payment, a strong co-applicant, or more documentation. The best approach is to keep all current payments clean and show stable income and a low existing EMI burden for a sustained period.

How long will “written-off” or “settled” stay in my credit report?

Credit information must be retained for at least 7 years as per TransUnion CIBIL’s stated retention requirement under the CICRA context. The impact reduces over time if you build a clean repayment track record, but the remark can remain visible.

Can I change “settled” to “closed”?

Only if the lender agrees and you pay the remaining dues as per their calculation, and they update the bureau reporting accordingly. There is no magic button at the bureau level. Start with the lender, get it in writing, then track whether it reflects in your report.

What should I do if my report shows “written-off”, but I paid the loan?

Raise a dispute with the bureau and share your payment proof and closure letter. CIBIL notes dispute resolution may take around 30 days, depending on the lender’s response. Also, email the lender’s grievance team so they can correct the reporting from their side.

Conclusion

If you remember one thing, it’s this: Closed is clean, settled is a compromise, written-off is a major red flag. These statuses can affect your future loan approvals and interest rates, even if your salary is good today. The practical approach is to verify your report, correct errors promptly, and rebuild trust through consistent repayments.

Next step: check your report, identify any settled or written-off accounts, and decide whether you can move towards “paid in full” or focus on 6–12 months of clean repayment behaviour.

Check your credit score and report regularly to catch these issues before your next loan application.