Loan Restructuring in India: When to Ask, How It Works, and Credit Score Impact

Loan restructuring sounds scary, but in many Indian households, it’s simply a way to avoid a full-blown default when cash flow gets tight. It means you and the lender agree to change the loan terms so your monthly payment becomes manageable. This could mean a longer tenure, a lower EMI for some time, or a revised repayment schedule. The most important thing is timing. If you wait too long and miss multiple EMIs, your options narrow, and credit damage worsens. If you act early, restructuring can protect you from penalties, repeated calls, and long-term eligibility issues. In this guide, you’ll learn when restructuring makes sense, how it usually works in India, how it can show up in your credit report, and what to do next so your future home loan or personal loan plans don’t get blocked.

Quick answer

Loan restructuring is a lender-approved change in your loan terms to reduce EMI stress during genuine financial difficulty. It can help you avoid default, but it may show up in your credit report as a restructured account, and lenders may treat it as a caution signal. Clean repayments after restructuring matter the most.

What is loan restructuring?

Loan restructuring is a formal change in loan terms agreed between you and the lender because you’re facing repayment difficulty. It may include extending the loan tenure to reduce EMI, temporarily reducing EMI, changing the repayment schedule, or revising the terms in line with the lender’s policy. This is not an informal promise made on the phone. RBI has frameworks and reporting expectations around such changes, so lenders typically follow a defined process.

When should you ask for restructuring?

Ask early, ideally before the first missed EMI. Restructuring is intended for real stressors, such as job loss, pay cuts, salary delays for a sustained period, major medical expenses, or irregular income phases for self-employed borrowers. It also makes sense when you can see a recovery path in the next few months, but need breathing space right now. Avoid restructuring if you can manage by cutting discretionary spending for 2–3 months, or if you’re doing it just to free money for lifestyle spending. Also, if you’re planning a big loan soon, like a home loan, the cleanest profile is always better, so restructure only if it’s genuinely required. The simplest rule is this: if paying EMIs is forcing you to miss essentials like rent, groceries, school basics, or medicines, talk to the lender now, not later.

How loan restructuring usually works in India

Step 1: Reach out before EMIs start bouncing

Start with customer care, then move to email to build a written trail. Share your problem clearly and ask what relief options are available under their policy.

Step 2: The lender checks your situation

Most lenders ask for basic proofs like salary slips, bank statements, or income proofs, and a short explanation of why you’re facing stress. They’re trying to see if the issue is temporary and whether you’ll be able to follow the revised plan.

Step 3: The lender offers revised terms

Common changes include tenure extension so EMI reduces, a revised schedule, or in some cases a temporary relief structure depending on the lender and the loan type. Don’t focus only on EMI. Ask for the total cost, too, because a longer tenure usually increases total interest.

Step 4: You accept, and the new plan becomes active

Once you accept, the lender treats the revised plan as your new repayment contract. Set auto-debit again if needed and keep a buffer balance so you don’t bounce under the new plan.

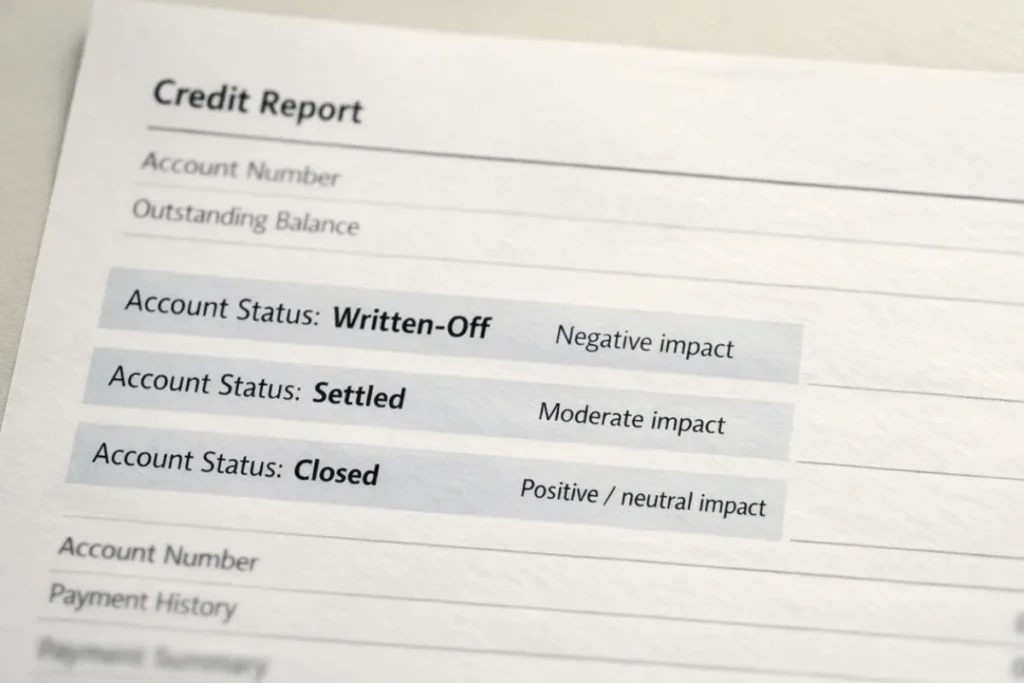

Credit score impact of restructuring

Restructuring can affect your future loan approval because it signals repayment stress at some point, even if you didn’t default. Lenders don’t treat it the same as “settled” or “written-off”, but it can still be a caution flag in underwriting. RBI has directions on how credit information is reported and maintained through credit information companies, which is why accuracy and lender confirmation matter when something is updated. What reduces the long-term impact is what you do after restructuring. If you consistently pay on time for the next 6–12 months, your profile will start looking stable again. If you restructure and then miss EMIs again, the damage becomes much bigger than the restructuring tag itself. Also, watch your credit card usage during this period. High utilisation plus a restructured loan makes your profile look stretched.

Restructuring vs other options

| Option | When it fits | What it signals | Risk level |

|---|---|---|---|

| Restructuring | Genuine temporary stress, want to avoid default | You cannot repay the full dues | Medium |

| Budget reset + buffer | Short mismatch, can recover quickly | You can manage without changing loan terms | Low |

| New loan to pay old EMI | Rarely sensible | You are stacking debt | High |

| Settlement | You cannot repay full dues | You didn’t repay in full | Very high |

Mini case example

Priya has a personal loan EMI of ₹22,000. Her salary drops for 6 months due to a job switch and probation. She realises she will start missing EMIs from next month. Instead of waiting, she emails the lender and shares updated salary slips and bank statements. The lender extends the tenure, bringing EMI down to ₹15,000. Her credit report later shows the loan as restructured, and after she pays every EMI on time, her overall profile stabilises. She avoids late fees, avoids deeper negative marks, and keeps future options open. The key was acting early and sticking to the revised plan.

Common mistakes to avoid

People often wait until 2–3 EMIs are already missed, then try to negotiate. That reduces options. Another mistake is treating restructuring as “free relief” while continuing to overspend, which leads to a second default. Many borrowers accept new terms without checking the total interest cost, then feel cheated later. Some don’t check their credit report after restructuring, so reporting errors remain unnoticed. If any information is wrong, CRIF High Mark provides a consumer dispute flow, but corrections usually require lender confirmation, so lender follow-up is essential.

Practical checklist before choosing restructuring

- Check if you can recover with a tight budget for 2–3 months; if not, talk to the lender now

- Ask for revised EMI, revised tenure, and total amount payable under the new plan

- Confirm if there are any fees or charges for the change

- Get the revised plan confirmation via email

- Reset auto-debit and keep a 10–15 day buffer in your account

- After the first month, review your credit report to ensure the account is being reported correctly

- If you spot errors, raise them with the lender first, then use the CRIF dispute route with documents if needed

FAQs

Is loan restructuring the same as settlement?

No. Restructuring changes repayment terms so you can continue paying. Settlement usually means paying less than the total dues as a compromise, which is viewed more negatively for future loans.

Will restructuring stop recovery calls?

If restructuring is approved and you follow the new plan, calls typically reduce because the account is regular again. If payments are still missed, calls can restart.

How long does restructuring affect loan eligibility?

There is no fixed number of months. Lenders usually care most about recent behaviour. Clean payments for 6–12 months after restructuring improve your profile.

Can home loans be restructured in India?

Depending on lender policy and RBI frameworks, restructuring can be offered in genuine difficulty cases. The exact relief type varies by lender and loan type.

What if my credit report shows the wrong restructuring status?

Start with the lender and ask them to correct the reporting. If it still doesn’t get fixed, use the CRIF High Mark dispute process with supporting proof.

Conclusion

Loan restructuring is not a shortcut; it’s a safety tool when your EMI is genuinely becoming unmanageable. If you act early, understand the revised cost, and repay on time after restructuring, you can avoid deeper credit damage and keep future loan options open. A practical next step is to map your monthly essentials, estimate how long the stress will last, and contact your lender before you miss an EMI. Also, check your credit report after the change so errors don’t silently hurt you later.