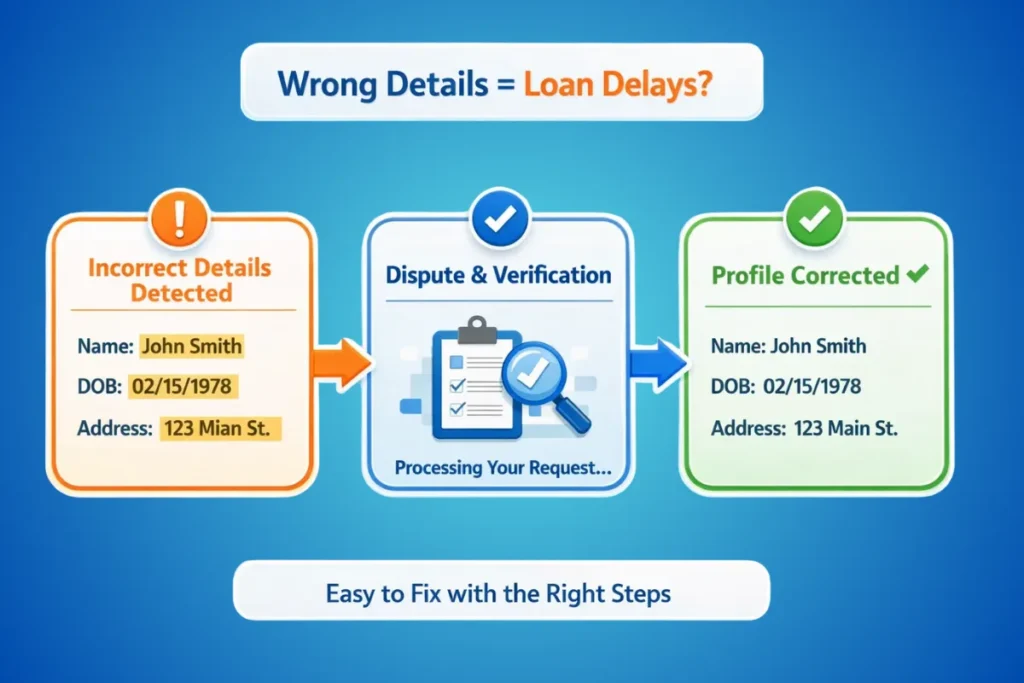

Wrong personal details in your credit report (name, DOB, address) can absolutely affect loan approvals in India, even if your repayments are perfect. Many lenders do an automated match of your application details with your credit report and KYC data. If the match fails, your application may be delayed, flagged for additional verification, or even rejected.

What “wrong personal details” look like

Common issues people see:

- Name spelling mismatch (Amit Kumar vs Amit K)

- Wrong date of birth (digit swap or old record)

- Old or unknown address showing as current

- Phone number or email that you have never used

These errors usually occur because lenders report data in monthly batches, and sometimes old KYC or incorrect entries are shared across systems.

Does it affect loans and credit score?

It may not reduce your score directly, but it can affect loan and card approvals because:

- KYC and identity checks become harder

- Lenders may suspect a duplicate profile or fraud

- Your credit file may not match correctly with PAN and application details

If you see an address you never lived at, treat it seriously and verify if any unknown account is also showing.

Quick checklist before you raise a dispute

Before you click “dispute”, do these 3 things:

- Download your latest credit report and note exactly what is wrong (field, value, and bureau).

- Check if the “wrong” address is actually your old rented house or hostel address. Old addresses sometimes remain as history, and that’s okay.

- If any loan or card appears unfamiliar or contains incorrect details, pause and treat it as a possible identity issue.

To keep your credit score clean, regularly check your credit score and review the report section that lists personal details and enquiries.

How to correct a wrong name, DOB, or address

Here’s the clean step-by-step process that works in most cases.

Step 1: Collect proof documents

Keep clear scans of:

- PAN (for name)

- Aadhaar or passport (for DOB and address)

- Any supporting document, like a recent utility bill for the current address

Step 2: Raise a dispute with the credit bureau where you saw the error

Most bureaus let you submit disputes online to correct personal information.

- TransUnion CIBIL allows consumers to initiate disputes online for inaccuracies in their personal and contact information.

- CRIF High Mark has a portal flow where you select the report and raise a query, including personal and contact details.

- Equifax India also provides a consumer dispute flow for updating credit report details, including personal information.

Fill in the dispute carefully. Select the exact field (Name, DOB, or Address) and upload proof.

Step 3: Raise the same correction request with the lender

This is important. Credit bureaus usually verify disputed data with the lender who reported it. If the lender updates their records faster, your fix becomes smoother.

Send the lender:

- Loan or card reference (if applicable)

- Your PAN

- Correct details and proof

Ask them to correct their internal KYC and “report updated data to the credit bureau”.

Step 4: Track the ticket and follow up

You’ll get a dispute ticket or reference number. Save it. Most disputes are resolved in a few weeks, and many platforms mention a typical window of around 30 days, depending on verification.

If nothing changes after 30 to 45 days, follow up with both the bureau and the lender using the same ticket trail. Thoda patience lagta hai, but it works.

Mistakes to avoid

- Disputing everything at once without proof. Keep it specific.

- Applying for a new loan while your identity details are mismatched. Wait till it’s corrected.

- Ignoring unknown addresses. If it’s truly unfamiliar, investigate properly.

FAQs

1) Will a wrong address in my credit report reduce my score?

Usually no, but it can create verification issues during loan approval and may signal a data mismatch.

2) How long does it take to correct a name or DOB in a credit report?

Often, a few weeks, and many dispute processes mention timelines of around a month, depending on lender verification.

3) Should I dispute an old address that I lived at earlier?

Not necessary. Old addresses can remain as history. Dispute only if it’s wrong or unfamiliar.

4) Do I need to contact the lender or only the bureau?

Do both. The bureau typically validates through the lender, so lender-side corrections speed up the process.

5) What if my details are correct in KYC but wrong in the credit report?

Raise a dispute with proof and ask the lender to update what they have reported. This usually resolves it.